The Logistics of Cross-State Inheritances: What to Do When a California Will Faces Texas Probate

When a California estate includes Texas real estate, the family must connect the California probate record to Texas law and the Texas county records.

Most families assume that once a California probate court admits the will and appoints an executor, the executor can handle every asset the deceased person owned. That is a reasonable assumption. It is also where many cross-state estates first get stuck.

A California probate case controls the administration of a California resident’s estate, but it does not automatically create an insurable chain of title for a house, ranch, vacation property, or rental located in Texas. Real property is governed primarily by the law of the state where the land sits. Texas therefore needs its own legally recognized link between the deceased owner, the California will, the person acting for the estate, and the person who will ultimately receive or buy the property.

That bridge is often called ancillary probate. In some cases, however, a family can use a narrower recording procedure instead of opening a full Texas administration. In other cases, the Texas property already passes outside probate because it was owned by a trust, held with survivorship rights, covered by a transfer-on-death deed, or owned through a business entity.

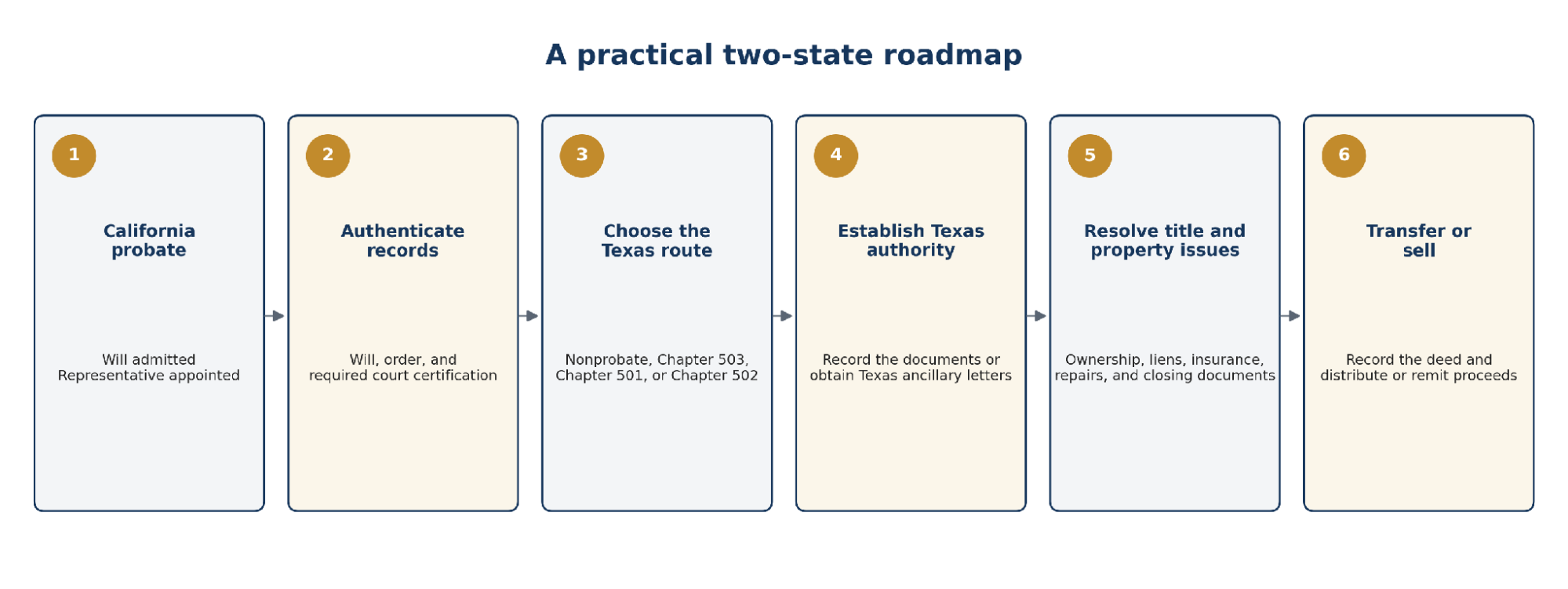

The first lesson is simple: do not decide the procedure from the word ‘will’ alone. Start with the Texas deed, the California probate record, and the practical goal for the property. Then let the Texas probate attorney and title company determine which route produces a clean, marketable title with the least unnecessary court involvement.

| Important: This article provides general educational information about cross-state probate and inherited Texas real estate. It is not legal, tax, title, or notarial advice. The correct procedure depends on the deed, will, trust, California court record, Texas county, liens, family circumstances, and title-underwriting requirements. A Texas probate attorney and the title company handling the property should approve the plan and every recordable document before anyone signs. |

|---|

Table of Contents

- 1. Why one estate can require two state processes

- 2. Start with the Texas deed, not the California will

- 3. The four possible Texas pathways

- 4. How ancillary probate works in Texas

- 5. The document packet Texas actually needs

- 6. From probate authority to an insurable title

- 7. How mobile notaries public can facilitate the transaction

- 8. Avoiding dual-state legal and logistical logjams

- 9. A practical 30-day coordination plan

- 10. Tax and valuation issues that should not wait

- 11. Frequently asked questions

Why One Estate Can Require Two State Processes

California calls the main proceeding the administration of the decedent’s estate. Texas calls the added proceeding ancillary because it is secondary to the probate in the state where the person was domiciled. The word ‘foreign’ in the Texas Estates Code also causes unnecessary confusion. In this context, a California will is a foreign will even though it comes from another U.S. state, not another country.

California probate establishes the will, identifies the personal representative, gathers the estate, addresses claims, and distributes property under California law. California’s court system describes probate as the legal process used to transfer property after death and to appoint the personal representative who collects assets, pays bills, and distributes what remains. [5]

Texas has a separate concern: the Texas land records must show a legally sufficient path from the deceased owner to the next owner. Chapter 501 of the Texas Estates Code allows a will of a person who was not domiciled in Texas to be admitted to ancillary probate when the will affects Texas property and has already been probated or otherwise established in another state. [1]

This does not mean the family is starting the entire estate over. Texas is generally dealing with the Texas property and the authority needed to manage or transfer it. The two proceedings should be coordinated, but they do not perform identical jobs.

The cross-state process works best when the California court record, Texas probate procedure, title work, and closing documents are treated as one coordinated project.

Start With the Texas Deed, Not the California Will

Before anyone orders court copies or files a Texas application, obtain the most recent recorded deed for the Texas property. The deed often answers the most important threshold question: did the deceased person own the property individually, or did the property already have a nonprobate transfer mechanism?

| How title appears

|

Likely consequence

|

What to verify immediately

|

|---|---|---|

| The decedent’s individual name | A Texas probate or foreign-will recording procedure is often needed before title can be transferred. | Exact legal name, marital status, legal description, liens, and whether the will specifically disposes of the property. |

| A revocable living trust | The successor trustee may be able to convey the property without probate if the deed and trust were properly completed. | Trust name and date, trustee succession, certification of trust, and title-company requirements. |

| Joint ownership with survivorship language | The surviving owner may take outside probate, but recording documents are still usually needed. | The deed’s exact survivorship language, death certificate, and any required affidavit. |

| A transfer-on-death deed | The named beneficiary may receive the property outside probate if the deed was valid and not revoked. | Recording date, beneficiary identity, death certificate, debts, and title-company underwriting. |

| An LLC, corporation, or partnership | The entity still owns the land. The estate may own an interest in the entity rather than the real estate itself. | Governing documents, ownership records, manager authority, and whether the entity remains active. |

| Co-ownership without survivorship | Only the decedent’s undivided interest enters the estate; the surviving co-owner does not automatically receive that interest. | Percentage ownership, community-property issues, liens, and the intended disposition under the will. |

A common and expensive mistake is assuming that a trust controls the property because the will contains a pour-over clause. A pour-over will may direct probate assets into a trust, but it does not retroactively place real estate into the trust during the owner’s lifetime. The recorded deed still matters.

The same principle applies to an LLC. If a California resident owned all membership interests in a Texas LLC and the LLC owned a ranch, the land itself may not be a probate asset. The estate may need to transfer or administer the LLC interest instead. That can avoid ancillary probate of the land, but it creates a different set of company, tax, and authority questions.

Do Not Overlook Severed Mineral, Royalty, and Wind Interests

A family may discover that the decedent no longer owned the surface house or ranch but still owned a severed mineral interest, royalty interest, overriding royalty, production payment, or oil-and-gas lease interest. Texas law treats minerals in place and many royalty interests as interests in land or mineral property. They can therefore create the same cross-state title problem as a house or acreage tract. [12]

Do not assume that small royalty checks mean the ownership is simple. A payor may place proceeds in suspense when there is a title dispute, reasonable doubt about the payee’s ownership, or an unmet title requirement. The family may need an authenticated probate record, a recorded transfer, curative deeds, or other evidence before the payor will update its division order and release funds. [13][14]

Wind-energy interests require separate document review. Texas has not fully defined wind and solar rights in the same way it has defined the oil-and-gas mineral estate. Wind payments are often created through recorded leases, easements, surface-use rights, and contractual payment provisions. A Texas attorney and title professional should examine the specific instrument rather than treating a wind interest as automatically identical to a mineral royalty. [15]

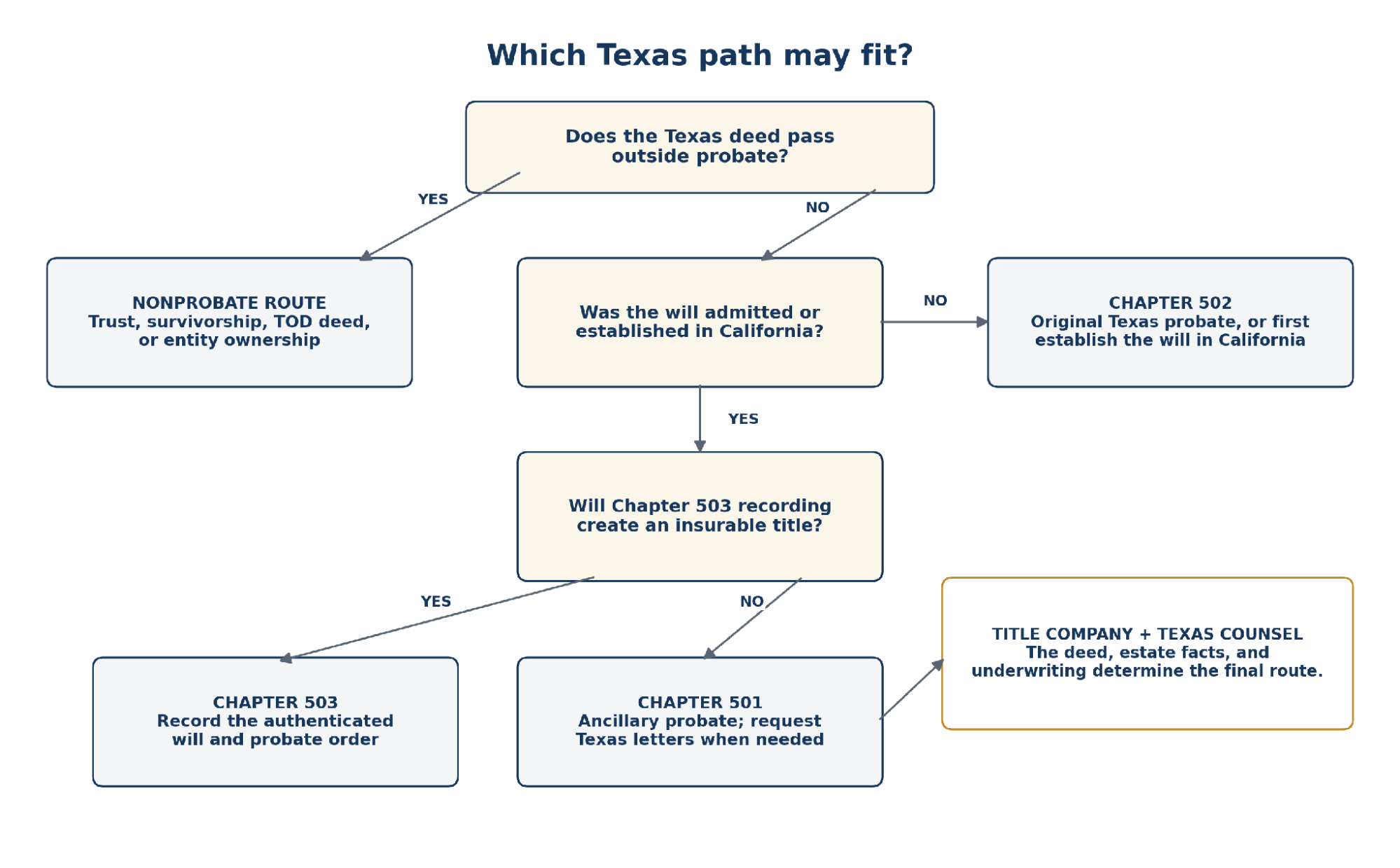

The Four Possible Texas Pathways

Texas law offers more than one route. The correct choice depends on how the property is titled, whether the will has already been established, whether active Texas administration is needed, and whether the title company will insure the proposed transfer.

| Selected pathway

|

Best-fit scenario

|

Core outcome

|

|---|---|---|

| Nonprobate transfer | Property is validly held in an active living trust, under a survivorship deed, through a transfer-on-death deed, or by an entity. | Can bypass probate of the land when the transfer mechanism is complete and the title underwriter accepts the supporting documents. |

| Chapter 503 deed-record filing | The California will and probate order directly distribute the Texas property and no local administration is needed; it can also support a Chapter 505 sale when the will gives the foreign executor or trustee an express power of sale. | The authenticated will and order are recorded in the county deed records and can operate as a conveyance and notice of title. [2][10] |

| Chapter 501 ancillary probate | The will was probated in California and Texas probate-docket recognition is needed, but no ongoing local administration is required. | The foreign will is considered admitted in Texas and receives the same effect as a Texas-probated will, subject to the statutory contest process. [1] |

| Chapter 501 plus ancillary letters | The California executor must actively manage, sell, litigate over, or otherwise administer the Texas property. | An eligible foreign executor can obtain Texas ancillary letters and full local representative authority for the matters those letters cover. [1] |

Chapter 502 is a separate fallback rather than one of these four will-based pathways. It permits an original Texas probate of a qualifying nonresident’s will when the will has not already been admitted or otherwise established in another jurisdiction. That route may require more proof, notice, and court involvement. [3]

The simplest route on paper is not always the simplest route at closing. A Chapter 503 recording can be legally effective, yet a title underwriter may still require an ancillary proceeding, additional affidavits, beneficiary joinders, or a deed signed by a particular party. That is why the title company should be involved before the Texas filing, not after the family has already committed to a path.

An Additional Intestacy Alternative: Affidavit of Heirship

When a California resident died without a will, or when probate is no longer practical, a Texas title company may consider an Affidavit of Facts Concerning the Identity of Heirs under Estates Code Chapter 203. The affidavit is recorded in the deed records of the county where the Texas land is located and supplies sworn family-history facts that can be used as nonjudicial evidence of heirship. [11]

The affidavit is not a court order and does not itself operate as a deed. Under Section 203.001, its statutory prima facie evidentiary effect arises after it has been recorded for five years, and it does not prejudice an omitted heir or creditor. Texas title practice often requests affidavits from two knowledgeable, disinterested witnesses, but the exact affidavits, deeds, waiting period, and supporting records are underwriting decisions. The title company must approve the approach before the family relies on it for a sale. [11][16]

This is a planning framework, not a substitute for legal or title advice. Title underwriting and the facts of the estate determine the final route.

How Ancillary Probate Works in Texas

The Texas ancillary process is often more focused than families expect, but the notice rule depends on where the will was established. When a California resident’s will was admitted in California – the decedent’s domiciliary jurisdiction – Section 501.003(a) says citation or notice is not required for the Chapter 501 application. If the will was established in a jurisdiction other than the decedent’s domicile, Section 501.003(b) requires citation by a qualified delivery method to each devisee and heir identified in the application. [1]

- Confirm domicile and the status of the California case. Texas Chapter 501 applies when the person was not domiciled in Texas and the will has been admitted or otherwise established in another jurisdiction. If there is a dispute over whether California or Texas was the person’s true domicile, stop and obtain legal advice before filing.

- Select the proper Texas venue. For a nonresident who died outside Texas, Section 33.001 can place venue in a Texas county where the nearest of kin resides or, if there is no qualifying Texas next of kin, where the principal Texas estate was located. Do not assume the property county is automatically the only permissible venue. [4]

- Obtain the authenticated California probate packet. Texas requires more than an ordinary photocopy and may require more than the certified copy a family routinely orders online. The packet must include the will and the judgment, order, or decree establishing it, with the clerk’s original attestation, the judge’s certificate that the attestation is in proper form, and the court seal if one exists. [1]

- File the Texas application. If the will was probated in California as the decedent’s domiciliary state, the application proceeds under Section 501.002(a) without citation or notice. If the will was established in a different jurisdiction under Section 501.002(b), the application must identify the devisees and heirs so the clerk can issue the required citation and service. [1]

- Have the clerk make the Chapter 501 probate-docket recording. For a will established in the domiciliary state, Section 501.004 makes recording the authenticated will and proof a ministerial duty of the clerk and expressly says that a separate court order is not necessary for that recording. This is different from Chapter 503, which places the authenticated will and probate order in the county’s real-property deed records. Once the Chapter 501 documents are properly filed and recorded, the foreign will is considered admitted in Texas and has the same effect as if the original had been admitted by a Texas court, subject to the statutory contest process. [1][2]

- Request ancillary letters only when they are needed. The California executor may apply for Texas ancillary letters testamentary by proving that the executor qualified in the original jurisdiction and is not disqualified in Texas. If the Texas filing occurs more than four years after death, the executor must still be serving in the original jurisdiction. [1]

- Complete the title work and transaction documents. The probate filing does not erase mortgages, judgments, tax liens, ownership discrepancies, missing releases, homestead claims, or defects in prior deeds. The title company still has to underwrite the Texas property and specify who must sign the deed and closing documents.

One useful feature of Texas law is that a foreign will admitted in the decedent’s domiciliary jurisdiction can dispose of Texas property even if the will was not executed with the formalities Texas would normally require for a Texas will. [1] That recognition prevents families from having to re-prove a valid California will under a different set of execution rules merely because the decedent owned property here.

The Document Packet Texas Actually Needs

The most avoidable delays in ancillary probate come from ordering the wrong documents. Families often request a certified will and a certified order, send them to Texas, and discover that the certification does not satisfy the authentication language in Section 501.002. Throughout this guide, the term authenticated copy means the statutory court packet containing the clerk or records custodian’s attestation, the judge or presiding magistrate’s certificate that the attestation is proper, and the court seal if one exists. The safest approach is to send those exact requirements to the California probate clerk before placing the order instead of relying on informal copy labels. [1]

| Document

|

Why Texas needs it

|

Frequent problem

|

|---|---|---|

| Certified death certificate | Confirms death and supports title, insurance, tax, and closing requirements. | The name does not match the deed, or the family orders too few originals. |

| California will and codicils | Shows the dispositive plan, executor nomination, powers, and specific treatment of the Texas property. | A codicil is omitted, pages are incomplete, or the copy is not tied to the probate record. |

| California order admitting the will | Proves that the will was established in the domiciliary proceeding. | The family submits letters alone without the order or judgment establishing the will. |

| Authenticated court packet | Satisfies Texas requirements for clerk attestation, judicial certification, and seal. [1] | The packet is merely file-stamped or ordinarily certified rather than authenticated in the required form. |

| Current California letters | Shows that the representative is presently qualified and may support the request for ancillary letters. | The letters have expired for third-party purposes or do not reflect a successor representative. |

| Texas deed and legal description | Identifies the exact land and the record owner. | The street address is used instead of the legal description, or the deed is not the latest deed. |

| Trust or entity documents | Determines whether the land is actually a probate asset and who has authority to act. | The family assumes ownership based on a will without checking the deed or entity records. |

| Preliminary title commitment or title report | Reveals liens, restrictions, ownership gaps, and the underwriter’s probate requirements. | Title work starts only after a buyer is under contract. |

| Date-of-death valuation | Supports tax basis, fiduciary decision-making, and later gain calculations. [9] | No retrospective appraisal is obtained because the family does not plan to sell immediately. |

From Probate Authority to an Insurable Title

Probate authority and insurable title are related, but they are not the same thing. A Texas court can recognize the California will, yet a title company may still refuse to insure a sale until every ownership and lien issue is resolved.

Chapter 503 illustrates the distinction. It permits an authenticated foreign will and the order admitting it to probate to be recorded in the deed records of a Texas county where the land is located. Once delivered for recording, the documents can take effect as a deed of conveyance for the property covered by the instrument and provide notice of the title conferred by the will. [2]

That can be an efficient solution when the will gives the property directly to a beneficiary and no active Texas administration is required. But a sale introduces additional questions: Who is the grantor? Does the executor have a power of sale? Did title vest in the devisees? Are all beneficiaries competent and available? Does a surviving spouse have rights that must be addressed? Are there creditors, liens, or contested claims? The title company will answer those questions through its underwriting requirements, usually with input from Texas counsel.

When a Foreign Executor May Sell Under Chapter 505

Texas Estates Code Section 505.052 provides a narrower power-of-sale route. If the authenticated foreign will has been recorded in the Texas county deed records under Chapter 503 and the will expressly gives the executor or trustee power to sell Texas property, the foreign executor or trustee may convey the property without a separate Texas court order authorizing that sale. Any directions or limitations in the will still control. [2][10]

This provision can eliminate the need for Texas ancillary letters in an appropriate sale, but it is not automatic. The will must actually contain the power, the Chapter 503 recording must be sufficient, the person signing must still hold the relevant foreign office, and the title underwriter must approve the deed, capacity, and supporting evidence. A California appointment by itself is not enough.

The practical rule is to obtain a preliminary title review early. Waiting until the property is under contract puts the estate on the buyer’s timetable. Early title work allows the family to correct name variations, locate unreleased liens, resolve a trust or entity mismatch, and choose the probate route before a closing date is at risk.

How Mobile Notaries Public Can Facilitate the Transaction

Cross-state estates generate signatures in several places at once. The executor may be in Los Angeles, one beneficiary may be in Sacramento, another may be in Texas, and the property may be in Kendall, Comal, Bandera, or Bexar County. Requiring every signer to travel to the title office is usually unnecessary.

A mobile notary public can travel to the signer, verify identity, witness the required acknowledgment or oath, complete the notarial certificate, and help return the signed originals. OneNotary’s mobile service is designed to coordinate in-person notarizations across U.S. ZIP codes, which can be useful when an executor, heir, or trustee cannot easily reach a title office. [8]

Mobile notarization is particularly useful for executor’s deeds, beneficiary deeds, affidavits affecting title, closing packages, consents, certifications, and other documents that the Texas attorney or title company has already prepared. Texas generally permits a recordable property instrument to be recorded when it has been acknowledged, sworn to with a proper jurat, or otherwise proved according to law. [6] Texas also permits acknowledgments of written instruments to be taken outside Texas by a notary public, which is what makes an in-person California mobile notary workable for many Texas real estate documents. [7]

What the Mobile Notary Should Not Be Asked to Do

- Choose whether the estate should use Chapter 501, Chapter 502, or Chapter 503.

- Decide who has authority to sign or what capacity should appear in the signature block.

- Select or rewrite the notarial certificate without instructions from the document recipient or authorized legal professional.

- Certify the California probate court record. The court clerk, not the mobile notary, must provide the authenticated will and order required by Texas law.

- Give legal advice about the will, deed, trust, title, taxes, creditor claims, or distribution of proceeds.

A Clean Signing Workflow

- The Texas attorney and title company finalize the document and confirm the exact notarial certificate.

- The signer receives instructions not to sign before meeting the notary.

- The mobile notary confirms acceptable identification, appointment logistics, witness requirements, and whether wet-ink originals are required.

- The notary witnesses the signing and completes the certificate exactly as instructed.

- A scan-back is reviewed before the original is shipped by a trackable method.

- The title company confirms receipt and recording before the estate treats the transfer as complete.

Remote online notarization may also be available for some documents, but it should never be assumed. The commissioning state of the online notary, the location of the signer, the receiving county’s recording rules, lender requirements, and title underwriting all matter. The attorney and title company should approve the method before the document is signed.

Avoiding Dual-State Legal and Logistical Logjams

Cross-state estates rarely fail because of one dramatic legal issue. More often, they lose weeks through small coordination failures: the wrong court certification, a title search ordered too late, a beneficiary signing in the wrong capacity, an insurance policy lapsing, or the California and Texas professionals working from different assumptions.

| Role

|

Primary responsibility

|

Information that must be shared

|

|---|---|---|

| California probate attorney | Establish the will, maintain the domiciliary administration, obtain court documents, and confirm the representative’s status. | Will, codicils, orders, letters, inventory treatment, disputes, and expected distribution. |

| Texas probate attorney | Choose and complete the Texas legal procedure; prepare or approve probate and conveyance documents. | California record, Texas deed, title requirements, family objectives, and any contested issues. |

| Texas title company | Examine title, issue requirements, approve the signing party and deed form, and insure the transfer or sale. | Probate filings, deeds, liens, marital status, entity/trust documents, and closing instructions. |

| Property professional or local representative | Secure, inspect, maintain, document, and prepare the property while legal authority is being established. | Access, insurance limits, repair approvals, occupancy, utilities, and court or fiduciary restrictions. |

| Tax adviser or CPA | Address basis, income, estate reporting, expenses, and allocation of sale proceeds. | Date-of-death value, improvements, rents, carrying costs, sale costs, and distribution schedule. |

| Mobile notary | Execute approved notarizations at the signer’s location and return the documents correctly. | Final document, certificate instructions, identification rules, witnesses, scan-back, and shipping label. |

The Most Common Cross-State Failure Points

- The California probate is nearly complete before anyone checks how the Texas property is titled.

- The family orders ordinary certified copies instead of the authenticated court packet required by Texas Section 501.002. [1]

- The legal name on the California order does not match the Texas deed, loan, tax account, or trust documents.

- A California pour-over will is treated as proof that the Texas property was owned by the trust when the deed never transferred it.

- The family files in the most convenient Texas county without confirming statutory venue. [4]

- The estate lists the property before the title company determines who must sign the deed and what Texas authority is required.

- Wet-ink originals are mailed internationally or across the country without scan-back review or tracking.

- The property remains vacant without the insurer being told, or taxes, utilities, lawn care, security, and weather protection are ignored while the legal process continues.

- The family postpones a date-of-death valuation and later has no defensible basis record for tax reporting. [9]

- The deed search stops at the surface tract and misses severed mineral, royalty, or recorded wind interests that require a separate title update. [12][15]

- The family records an affidavit of heirship without first confirming that the title underwriter will accept it and specify the required witnesses, deeds, and supporting documents. [11]

A Practical 30-Day Coordination Plan

The following is a project-management sequence, not a promise about court timing and not a set of statutory deadlines. Its purpose is to get the legal, title, property, tax, and signing work moving in parallel instead of one step at a time.

| Planning window

|

Priority actions

|

Target result

|

|---|---|---|

| Days 1-3 | Secure the property; notify the insurer; obtain the deed, will, trust, death certificate, and California case information; identify all decision-makers. | The estate understands what is owned, who is acting, and what immediate property risks exist. |

| Days 4-10 | Engage Texas probate counsel; open preliminary title work; send Texas authentication requirements to the California clerk; order a date-of-death appraisal if appropriate. | The legal path and title issues are identified before documents are ordered or the property is marketed. |

| Days 11-20 | Receive and review the authenticated packet; resolve name or deed discrepancies; choose Chapter 501, 502, 503, Chapter 505 power-of-sale treatment, an affidavit-of-heirship approach, or a nonprobate route; prepare the Texas filing. | The estate has a procedure the attorney and title company both accept. |

| Days 21-30 | File or record the Texas documents; request ancillary letters if needed; begin approved property preparation; establish mobile-notary and original-document protocols. | Legal authority, title clearance, property management, and future signing logistics are aligned. |

The sequence changes when the will is contested, the executor has not qualified in California, the property is occupied, a business entity owns the land, or the title search reveals serious defects. Those cases require a tailored plan rather than a checklist.

Tax and Valuation Issues That Should Not Wait

Probate procedure answers who can act and how title can move. It does not answer the tax consequences of keeping, renting, distributing, or selling the property.

For federal income-tax purposes, the basis of inherited property is generally tied to fair market value at the date of death, subject to exceptions and alternate valuation rules. [9] A date-of-death appraisal can therefore matter even when the family plans to keep the property. Years later, reconstructing the value of a unique Hill Country ranch, acreage tract, or custom home can be difficult and expensive.

The estate should also track post-death repairs, capital improvements, insurance, taxes, utilities, management costs, rental income, and sale expenses. Some items affect taxable income, some affect basis, some are estate-administration expenses, and some are simply carrying costs. A CPA familiar with estates and multistate issues should classify them rather than relying on the real estate closing statement alone.

California and Texas also treat property, income, and residency differently. A sale of Texas property by a California estate or California beneficiaries can create filing obligations in more than one jurisdiction. The family should obtain tax advice before distributing all proceeds, especially when there are unresolved returns, rental operations, business entities, or a large gain.

Frequently Asked Questions

Does a California will automatically transfer a Texas house?

No. The will may control who should receive the property, but the Texas title records still need a legally recognized transfer path. That may be a nonprobate deed process, Chapter 503 recording, Chapter 501 ancillary probate, or another procedure.

Does every California estate with Texas property need a full second probate?

No. Some property passes outside probate, and Texas Chapter 503 may allow authenticated California probate documents to be recorded directly in the deed records. Other cases need ancillary probate but not an ongoing Texas administration. The title company and Texas attorney should choose the route.

What if the Texas property was supposed to be in a California living trust?

Check the Texas deed. If the trust is the record owner, the successor trustee may be able to transfer or sell without probate. If the individual remained the record owner, the pour-over will alone does not eliminate the need to address the property through probate or another authorized transfer procedure.

What if no probate was opened in California?

Chapter 501 ancillary probate generally depends on the will already being probated or otherwise established elsewhere. Texas Chapter 502 permits original probate of certain foreign wills when that has not happened, although the court may wait for proceedings in the domiciliary jurisdiction. [3]

Do the California executor and heirs have to travel to Texas?

Usually not for routine filings and signings. Attorneys can handle many court matters, and approved deeds, affidavits, and closing documents can often be signed before a mobile notary where the signer lives. A hearing, dispute, property inspection, or unusual title issue may still make travel useful or necessary.

Can a mobile notary provide the authenticated California court copies?

No. The California court clerk must issue the authenticated will and probate order. A mobile notary can facilitate signatures on approved estate, title, and closing documents but cannot convert an ordinary court copy into the authenticated judicial record Texas requires.

Can the Texas property be listed before ancillary probate is complete?

The estate can often obtain valuations, inspect the property, complete title work, plan repairs, and prepare marketing while the legal process is underway. Whether the property should be publicly listed or placed under contract depends on who currently has authority, the administration type, the will, court restrictions, and title-company requirements.

Can the California executor sign the Texas deed?

Possibly, but not merely because California letters exist. Under Section 505.052, a foreign executor or trustee may be able to sell without Texas ancillary letters when the authenticated will and probate order have been recorded in the Texas deed records under Chapter 503 and the will expressly grants a power of sale. Otherwise, the signer may need Texas ancillary letters or another title-approved source of authority. [2][10]

What if the decedent owned only Texas mineral or royalty interests?

Those interests still require a documented transfer. Severed minerals, royalty interests, overriding royalties, and similar interests can exist even when the decedent owned no surface property. Unresolved ownership may cause a payor to suspend distributions until title requirements are met. The attorney, land professional, operator or payor, and title examiner should coordinate the appropriate Chapter 501, 503, 505, deed, or other curative route. [12][13][14]

Can an affidavit of heirship replace probate?

Sometimes, particularly when a person died without a will and a Texas title underwriter accepts the nonjudicial evidence. The affidavit is not a probate judgment or a deed, its statutory prima facie effect generally requires five years of recording, and it does not bind omitted heirs or creditors. Obtain the title company’s written requirements before recording or signing a sale contract. [11][16]

How long does the Texas process take?

There is no reliable one-size-fits-all estimate. A clean case with the correct authenticated record, uncontested will, simple title, and coordinated professionals can move far more efficiently than a case involving missing documents, disputes, liens, trust mismatches, mineral interests, or multiple properties. The controllable variable is preparation, but court, clerk, title, and document-delivery timelines still vary by case.

What if the deceased owned Texas property in more than one county?

A single Texas probate proceeding may establish the will and representative’s authority, but deed-record documents may need to be recorded in every county where land is located. Chapter 503 expressly allows recording in each county containing the land. [2]

Is ancillary probate still possible more than four years after death?

Chapter 501 allows a qualifying foreign will to be admitted in Texas at any time, but ancillary letters requested after the fourth anniversary require proof that the executor continues to serve in the original jurisdiction. [1] Delays can still create title, evidence, tax, maintenance, and family complications, so the absence of a simple four-year bar is not a reason to wait.

The Bottom Line

A California probate order is not worthless in Texas. It is the starting point. Texas law provides several ways to recognize the will, record the testamentary transfer, use a foreign fiduciary’s express power of sale, and issue local authority when active administration is needed. Intestate and stale-title cases may also require a carefully underwritten affidavit-of-heirship or judicial-heirship solution.

The goal is not to create a second bureaucracy. It is to give the Texas title system a clear, defensible chain from the deceased owner to the person who can lawfully keep, transfer, or sell the property. Families avoid the worst delays when they do four things early: pull the deed, involve a Texas probate attorney, obtain preliminary title work, and order the California court record in the exact authenticated form Texas requires.

The human side matters just as much. Someone is usually handling grief, family expectations, a distant property, and two sets of professional instructions at the same time. A written plan, one shared document list, and local help for the property and signatures can turn a confusing two-state problem into a manageable sequence of steps.

Sources

- Texas Estates Code, Chapter 501 – Ancillary Probate of Foreign Will

- Texas Estates Code, Chapter 503 – Recording of Foreign Testamentary Instrument

- Texas Estates Code, Chapter 502 – Original Probate of Foreign Will

- Texas Estates Code, Section 33.001 – Probate Venue

- California Courts Self-Help Guide – Property After Someone Dies

- Texas Property Code, Chapter 12 – Recording of Instruments

- Texas Civil Practice and Remedies Code, Chapter 121 – Acknowledgments and Proofs

- OneNotary – Mobile Notary Service

- IRS Publication 551 – Basis of Assets

- Texas Estates Code, Chapter 505 – Powers and Duties of Foreign Executors and Trustees

- Texas Estates Code, Chapter 203 – Nonjudicial Evidence of Heirship

- Texas Estates Code, Chapter 358 – Matters Relating to Mineral Properties

- Texas Natural Resources Code, Chapter 91 – Royalty Payment Requirements

- Railroad Commission of Texas – Royalties FAQ

- State Bar of Texas – What Are Renewable Energy Rights?

- State Bar of Texas – Transferring Property After Death and Avoiding Probate Court

About the Author

Bill Ross is a Texas real estate professional and Certified Probate Specialist with Hill Country Homesteads Group, serving families, executors, administrators, and heirs navigating the sale of probate and inherited property. He provides practical real estate guidance throughout the San Antonio area and Texas Hill Country.

Bill can be reached at Bill@HillCountryHomesteads.com or (210) 294-9190. Additional probate real estate resources are available at texasprobatehomes.net.